Published:

February 25, 2026

Updated:

May 4, 2026

Government pressure, regulatory approvals in two countries, and past fraud controversies complicate Citigroup’s Banamex IPO. Here’s what investors should understand about policy risk, valuation uncertainty, and Mexico’s evolving banking landscape.

Citigroup Inc. (Citi) has had a longstanding presence in Mexico’s banking sector, primarily through its ownership of Banamex. Acquired in 2001 for $12.5 billion1, Banamex has played a key role in becoming one of Mexico’s oldest and most recognized financial institutions. Although a good idea, this asset has become more complex for Citi as regulatory, political, and market pressures have evolved. At the same time, Citi was facing its own internal challenges on a global scale.

Leading up to 2021, Citigroup was struggling with underperformance, outdated technology, and overall low efficiency. As a result, Citi appointed a new CEO, Jane Fraser, in 2021 to help restructure the firm. As part of Fraser’s transition, in 2023 Citi decided to cancel a $7 billion sale of its Mexican consumer unit (Banamex) and instead pursue an Initial Public Offering (IPO) in 2025. Citigroup has explored a dual stock listing in Mexico City and New York City but there is no confirmation as to whether this will occur2. Originally Citigroup was preparing to sell to a conglomerate, Grupo Mexico, but tensions emerged between the conglomerate and the Mexican President, Andres Manuel Lopez Obrador. The Mexican government demanded that Citigroup allow Banamex to remain in Mexican hands and the new owner cannot cut costs by laying off employees. This placed pressure on the deal and led to an eventual change of plans. Another reason the deal was called off was due to the Mexican government’s expropriation of part of Grupo Mexico railway, which spooked investors and raised serious concerns about the pending transaction with Citi3.

In politically sensitive markets, early government signals can constrain who is allowed to buy (e.g., preference that Banamex remain in Mexican hands, plus conditions like no layoffs and tax compliance) and lengthen layered regulatory approvals (Mexico + U.S.), raising the policy risk premium that investors price through a higher discount rate—often pressuring valuation even when the underlying asset is attractive

Since acquiring Banamex in 2001, Citi has invested over $2.5 billion in enhancing Banamex’s capabilities and infrastructure. Citi plans on continuing to operate only as a locally licensed banking business by utilizing its Institutional Clients Group (ICG). The carve-out has been taking place since Citi announced its plans for the Banamex IPO. Citi projected that the separation would be completed at the end of 2024 and that the IPO would happen in 2025.4

As of December 2024, Citi has officially separated its institutional banking business from its consumer businesses in Mexico. Banamex will have an IPO and will focus on consumer banking while Citi Mexico will continue to be helped primarily by Citigroup and will focus on corporate clients.5 Citi’s CEO, Jane Fraser, said about this success:

Although it is a success, this is not new for Citi as they have been working to exit consumer banking in over 14 different markets from Europe to Asia. Currently, Citi has completed nine of those closures and is working in Poland to complete a sale.

As far as the financial reports is concerned, Citi will continue to report business results until its stake falls below 50% at which point it will stop presenting the financial information. For the IPO, multiple regulatory and legal issues need to be addressed and authorized before the final steps can be taken for the IPO.7

To further complicate the impending IPO, at the beginning of 2025, the CFO, Mark Mason, of Citi, stated that they had many regulatory approvals to still fulfill for Mexico and the USA before anything else happened. Although Citigroup has made it very apparent that it hopes to launch the IPO as soon as possible, the market conditions and regulatory approvals have significantly slowed down the process.8

This article examines why Citigroup’s decision to take Banamex public is a pivotal moment for the financial markets, Citigroup’s global strategy, and Mexico’s economic landscape. It will explore the financial and strategic implications of the IPO, the potential economic impact on Mexico and international markets, the competitive landscape Banamex operates within, the challenges and risks surrounding the IPO, and the overall market and governmental response.

This impending IPO means a couple of things for Mexico and the Mexican market. As Citi decides to carve out the consumer banking sector in Mexico, this speaks towards the profitability of the consumer banking sector in Mexico and has the potential to influence investors’ opinion of the stability and potential of Mexico’s market. This could either leave Banamex in a worse position as Citi withdraws from consumer industry, or it could leave the consumer market in Mexico at a loss as foreign and local investors decide to withdraw, as Citi seems to believe there is no potential in this banking sector.

Even in what may seem like a worst-case scenario with Citi’s withdrawal, the opposite effect could also be true. Citi’s exit leaves a clean slate in Mexico’s consumer banking sector, creating an opening for new investors or a third party to acquire Banamex. This transition could be highly attractive, as the new majority owner would have the chance to reshape the business and potentially unlock significant profits.

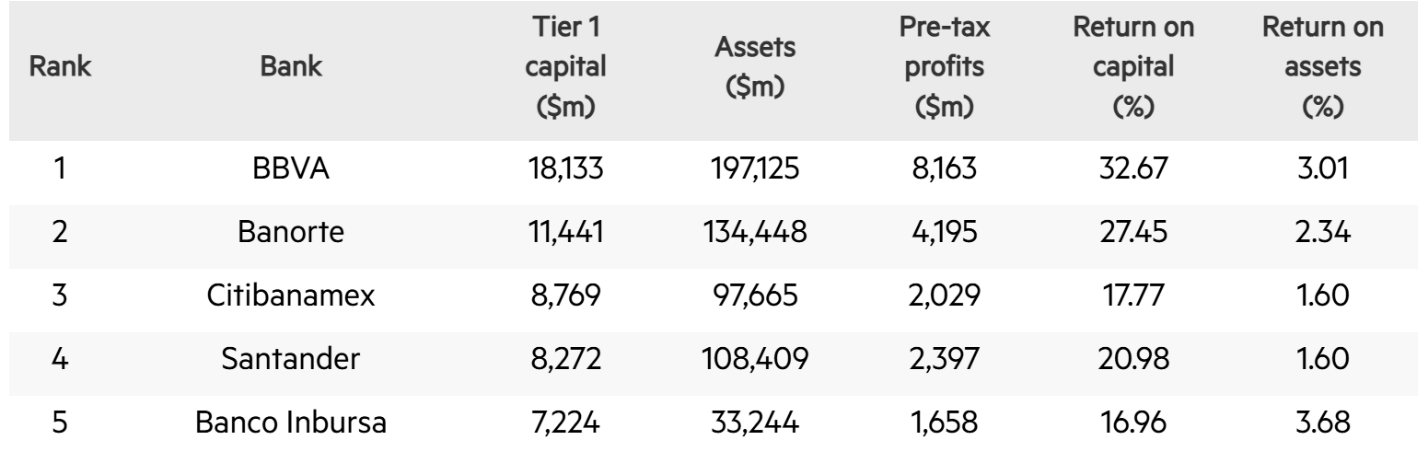

Banamex is currently the third-largest bank in Mexico, behind BBVA and Banorte 9(see Figure 1). Its performance is impressive, with pre-tax profits exceeding $2 billion and a return on capital of 17.17 cents for every dollar invested. This is among the highest in Mexico’s banking sector and highlights Banamex’s profitability. However, despite these strong results, Citi has chosen to divest. The reasoning lies in Citi’s broader global strategy: the bank sees higher long-term growth and efficiency in its Institutional Clients Group (ICG), which provides investment banking and services to corporations and governments. Compared to retail banking in Mexico, the ICG offers Citi greater scale, less regulatory friction, and more consistent returns. This explains why Citi opted to spin off Banamex, even though it remains a strong performer locally.

Figure 1: Top five banks in Mexico from The Banker Database

As far as how the IPO has affected the government, from the current news, we know that there are quite a few regulatory approvals that need to be met for the IPO to go through. Before the IPO was announced, the president of Mexico made stipulations when Citi was trying to sell to a conglomerate group, which could present as resentment towards Citigroup since they decided to move forward. The president was concerned about the bank remaining under Mexican ownership. If this is one of the president’s concerns, the president may disapprove of the possibility of the dual stock listing for the IPO. Despite this, the Mexican President, Andres Manuel Lopez Obrador, has stated that the Mexican government is interested in acquiring a significant stake. The ability to control Banamex is a benefit for the Mexican government and suggests that the IPO has been accepted by the Mexican government. The Mexican government has had significant influence over the IPO, which suggest that there will be a complex intertwining between corporate strategy and national interest.10

Considering the effects of the IPO on Citigroup and their future endeavors, the IPO will give Citigroup immediate gains as capital will pour in when the IPO occurs. Although the separation between Citi Mexico and Citi Banamex has already taken place, there will be a book value adjustment as Citigroup adjusts its books to reflect the IPO offering. With the IPO offering, Citigroup will continue its global simplification. As mentioned above, Citigroup has decided to close many of its global offices to focus on institutional operations and wealth management in markets of their choice. The exit from retail banking also helps Citigroup reduce complexity and concentrate on the chosen operations, but on the opposite side, they lose their foothold in Mexico in the retail banking. The IPO could lift Citigroup’s stock price as cash reserves gets inflated from the sale; however, any delay or challenges with the IPO could create uncertainty and negatively affect investor confidence. Long-term success will depend on how Citigroup reinvests the IPO proceeds to drive growth and innovation in its core business areas. The concern stems from disclosures in past financial statements, specifically noted in the Risk Factors section:

Specifically talking about Banamex in the risk section, this shows concern about Banamex and its ability to perform despite the money that has been dumped into it.

In two instances in the past, Banamex has committed fraud, which could have led to Citigroup ultimately deciding to let this retail section go. The first instance of fraud cited was in 2014 when a customer used fraudulent accounts receivable. Banamex had extended $585 million in credit, of which only $185 million was verified as valid. Citi charged the estimated loss to its 2013 operating expenses and initiated investigations, recovery efforts, and legal actions. Then in 2018, Banamex and others were sued for alleged collusion in Mexico's sovereign bond market. While the case was initially dismissed, the plaintiffs filed amendments, and litigation is ongoing under.13 Although Citigroup has not mentioned fraud as a reason for the IPO, it leaves investors wondering and possibly raises some concerns in the retail banking industry.

Even as Banamex is central to Citi’s strategic refresh14 to help streamline operations, reduce costs, and focus on high-return businesses, Citi’s exit from the retail market could significantly reshape Mexico's financial landscape, creating opportunities for other banks to fill the gap. For Mexican consumers and businesses, it may mean less competition, potentially higher banking fees, and fewer service options. On the positive side, Citi’s continued presence through the ICG may still support Mexico's larger financial infrastructure and institutional needs. The move also signals potential shifts in investor confidence and foreign investment in Mexico’s banking sector.

Last, when considering Banamex as a separate entity from Citigroup, Global S&P came out with ratings on how this separation affected how Banamex is rated globally. They discussed the high concentration of business activities and the low market share which makes them “…less resilient to adverse operating conditions than its larger rated dominated peers.”15 S&P estimates that Banamex’s market share of loans and deposits will decrease by 4% and drop from the 4th largest bank in Mexico to the 7th largest bank in Mexico. These reasons are why they adjusted Banamex to adequate which shows Banamex’s potential weaknesses which again could drive risk averse investors away from the incoming IPO. S&P Global back this sentiment when they state:

However, Banamex's high share of unsecured loans in its consumer loan portfolio--about 70% through credit cards and personal loans—reflects a higher risk appetite than that of the Mexican banking sector.

Policy signals matter early: Watch for government preference that Banamex remain in Mexican hands, especially when paired with conditions like no layoffs and tax compliance, since these can narrow the buyer universe and reduce competitive tension.

Timeline is a valuation input: Track layered regulatory approvals (Mexico + U.S.), because delays increase execution risk and can raise the discount rate investors demand.

Structure shifts are signals: A move from direct sale to IPO / partial stake sales can indicate that policy constraints are reshaping the path to exit—changing both timing and valuation.

In conclusion, the upcoming Banamex IPO carries significant implications for both Mexico and Citigroup. For Mexico, the IPO could reshape the country's financial landscape, presenting both risks and opportunities. While Citigroup’s exit from retail banking may reduce competition and raise concerns about market stability, it also opens doors for new players to capitalize on Banamex’s established brand and client base. For Citigroup, the IPO represents a critical step in its strategic shift toward focusing on institutional operations and high-return business areas. However, challenges such as regulatory approvals, investor concerns about Banamex’s market position, and historical issues of fraud add layers of complexity to the process. As Banamex prepares to stand alone, its ability to maintain profitability and adapt to market dynamics will determine its long-term success. Ultimately, this IPO serves as a pivotal moment for all stakeholders, marking a turning point for Citigroup’s global strategy and Mexico’s banking sector.